The Game of Equity Cash Out

Happy would be Tax Day everyone!

Normally, everyone remembers April 15th as Tax Day, or if you’re a Baseball fan, Jackie Robinson Day. With COVID-19 sending our country to unprecedented levels of caution, we all have an extra 90 days to file. For those that usually file an extension (myself included), I don’t believe we will get a 90 day extension (as of now). This post doesn’t have anything to do with taxes; yesterday I covered Property Taxes in Clark County and Tax Caps (read here).

Today, I want to talk about Home Equity, and how this time, once again, is different than last time. We’ve covered a lot of avenues when it comes to how this market is and will be different than the Great Recession. From Mortgage Rates, to market behavior during recessions, to Equity in homes…

This post is similar to the equity in homes post, where we discussed how more than 50% of the homes in the United States have at least 50% equity. You can read that post here. Today, we’ll cover what people are doing with their equity, or more accurately, what they are NOT doing with their equity.

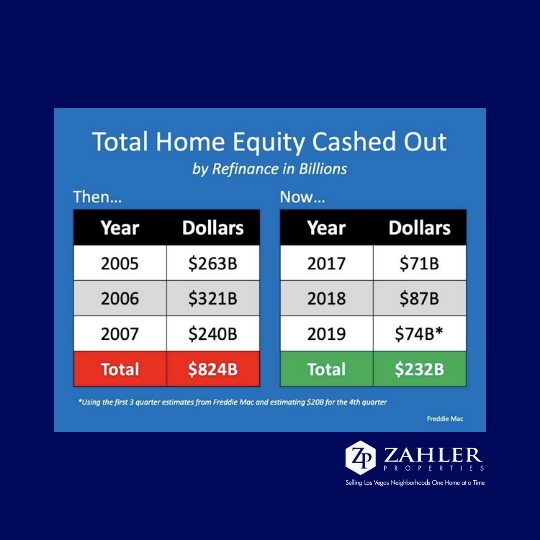

Back in 2005-2007, leading up to the crash, there was a total of $824 Billion (that’s $824,000,000,000) that was cashed out with Cash out Refinances in the United States. That equity was pulled OUT of peoples homes to be deployed other places; other investment property, boats, home improvements, vacations, etc. That is a LOT of money pulled out of homes, and a whole lot of homes that ADDED to their principal borrowed. Also, mortgage rates then were HIGHER than they are today. So people were adding to their balance on loan prices higher than today.

By comparison (and that’s what this post is about), The three year period we just had, 2017-2019, only saw a total of $232 Billion ($232,000,000,000)! That’s a SIGNIFICANT difference. In fact, this 3 year period TOTAL was less than the lowest year from the last cycle (2007 had $240B). The numbers do have a small estimate for 2019 as the first three quarters added up to $54 Billion, and they estimated $20 Billion for Q4, which would be in line with expectations.

We also know that Equity has consistently risen over the last 3 years! In fact, just using statistics in Las Vegas, property values overall (Single Family, Townhomes, Condos) have increased by roughly 35.5% over this 3 year time frame, yet far less equity has been pulled out. This means that people have not only seen their property values INCREASE dramatically in the last 3+ years, but they are, less and less, pulling those funds OUT. They’re keeping them in the homes! This jives with the statistic I presented the other week saying that over 50% of homes in the US now have more than 50% equity!

What does this all mean? Pricing in our markets drop dramatically when there is NO demand. Demand drops when the supply of buyers is limited, either by income levels, or credit, or available cash. Also, prices drop when Sellers have no reason to hold onto a property, as when they have NO or NEGATIVE equity. That’s not the case now. People haven’t been leveraging themselves to the max. They have been holding the equity in their home, and as long as they can manage their payments, there will be no large drive to sell and sell quickly. When we have a ‘run on a bank’ like we did in the Great Depression in 1929, we saw too much demand for cash. Banks couldn’t provide it, and it shut down the system. In 2008, people, by the millions, couldn’t make their mortgage payments because of adjustments to their mortgages, driving MORE people to try to sell in a process that takes longer to do (A short sale is NOT quick). This put too much pressure on the system, and the market crashed.

We won’t have the same type of pressures this time. People have equity in their homes. If they need to sell, they’ll be able to sell, and sell in a ‘normal’ transaction, not with a bank deciding yay or nay. The panic level won’t be hit. The market, as I said, is different this time. What are your thoughts?

-GZ